Waste to Energy in Europe: Creating an Investment Buzz

Waste management is a hot topic again in Europe and this can be seen on many levels: the overall growth in the technology and service markets; the impact that legislation is having on regional waste management strategies; the glut of recent acquisitions in the market; and the increasing focus of the private investment community on the sector.

Waste management is a hot topic again in Europe and this can be seen on many levels: the overall growth in the technology and service markets; the impact that legislation is having on regional waste management strategies; the glut of recent acquisitions in the market; and the increasing focus of the private investment community on the sector.Importantly, waste management in Europe is no longer a haulage and disposal business. The legislative shifts of the past decade have seen major moves towards the implementation of advanced technology and innovative recycling solutions. With landfill finally being truly on the way out, there are genuine opportunities for investment in value-adding solutions.

In spite of the importance of waste minimisation schemes, as well as recycling and biological waste treatment, many local and regional authorities currently view waste to energy (thermal waste incineration with energy recovery) as the only viable large scale alternative to landfill.

As a result, there is a clear buzz in the market that is aimed at the waste to energy sector. Attractive investment opportunities are being identified at both an individual project level and at companies that are well positioned to exploit the projected market growth (service providers and technology developers).

With Europe’s waste to energy capacity expected to increase by around 13 million tonnes and almost 100 new plants to come on line by 2012, it is not difficult to see why.

The changing face of Waste to Energy

Across Europe, the public sector is the traditional owner of waste to energy (W2E) facilities. This is changing, as large-scale investment is required to construct newer, environmentally friendly facilities. It is equally true that the importance of being able to sell profitably the electricity/heat generated from such plants is driving the attractiveness of investment and favouring partnerships with utility companies.

This is combining with the fact that many operators are seeing opportunities to raise W2E gate fees as low cost landfill disappears. W2E facilities are increasingly becoming profitable cash generators in their own right.

The result is that private sector companies are taking a greater responsibility in the sector, although to date investors have been mainly from a background in utilities, engineering and/or technology.

At an operations level, the large waste management firms also play a very key role, especially where W2E plant operation is a part of a larger integrated waste management contract. The recent acquisition in September 2006 of Cleanaway UK Ltd by French giant Veolia is an example of the large global players continuing to snap up local players in high growth markets where they see a clear opportunity to drive value-added waste solutions. This followed the high profile acquisition of the UK’s Waste Recycling Group by the Spanish company FCC for £1.4 billion in early 2006.

Meanwhile, the UK market has also seen considerable attention from the investment community in recent years, the most recent being the sale of Cory Environmental by Montagu Private Equity to a consortium of infrastructure investors (ABN AMRO Global Infrastructure Fund, Finpro SGPS and Santander Private Equity) for £588 million. As well as being among the leading UK waste management services companies, Cory has recently entered the W2E market by winning the contract to develop London’s first river-served W2E plant at Belvedere.

The W2E market in Europe is growing and will continue to do so for at least 8 to 10 years. At the same time, public sector outsourcing is also on the increase and private sector capital is increasingly being sought.

Government-owned versus private WTE markets

The W2E services market supports about 200 to 250 players in 2007. Much of the reason behind this low number (low compared to other waste management service segments) is the use of large centralised facilities in many parts of Western Europe for the incineration of municipal solid waste (MSW). However the number of companies is expanding as the network of thermal units in many countries is expanded.

The majority of those active in the market are municipal-owned companies with a growing percentage of these being ventures with the private sector. Such private sector companies typically operate such facilities while also providing links with other areas of the waste market (W2E contracts are typically integrated with waste collection, transportation, treatment and final disposal). Their profile varies with some European markets, such as Denmark, to date retaining a strong public sector profile. However with costs for the construction of incinerators and their operation increasing this sector is assuming a steadily increasing profile.

With a high percentage of locally owned facilities, either direct or joint venture, the sector can be considered as highly fragmented. A number of multinationals have a strong national presence, as in France, while names such as Sita, Veolia, Remondis and TIRU are also active in a number of other national markets.

Increasing private sector involvement

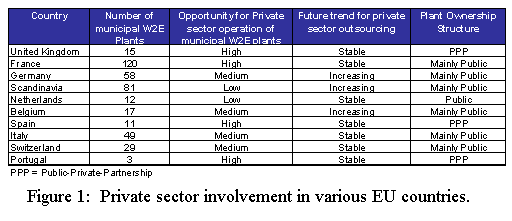

Figure 1 below shows indications of the level of private sector involvement in the operation of W2E facilities in the main European markets. Most countries have the private sector operation of at least some plants, although some in Northern Europe remain fairly committed to public sector management.

The bidding/tendering process for operation of plants (if the operation is to be outsourced) is almost always conducted at the same time as the tendering for the construction of the plant. As a result, build and operate contracts are common and many plants are operated by consortium companies.

The main private sector players in the market come from three main backgrounds and their relative presence varies by geography across Europe:

- The dedicated waste management players (e.g. Veolia, Sita, Remondis etc.) are strong across Europe, especially in the UK, France and parts of Germany. Core expertise is in the management of complex waste management contracts for cities and/or districts and the operation of W2E plants is commonly part of an integrated contract to manage the waste of a region.

- The civil engineering contractors (e.g. FCC, Cespa, Urbaser etc.) are especially strong in Southern Europe where they commonly form the main partner in a consortium to bring construction and operating expertise to infrastructure projects. Several of these engineering firms (FCC and Urbaser are good examples) have the capacity to make large investments, and also have dedicated waste management divisions or subsidiaries.

- The energy utility companies (e.g. EdF, EDP, RWE, Union Fenosa, etc.) play a big role in the countries where W2E is well established and the management of the energy/CHP facility is important. Many of the private sector consortia contain a utility partner. Indeed, EdF sees enough opportunity to have set up a dedicated subsidiary (TIRU) for W2E operations. Partnerships between TIRU and EdF are common across France and increasingly the rest of Europe.

The clear message is that the European waste management market is continuing to restructure and reform. The ongoing move away from landfill is continuing to attract technological innovation and the current leaning towards waste to energy in many parts of Europe is attracting major capital investment with improving opportunities for returns.

Frost & Sullivan expects significant growth in the European waste sector in the next 5 to 10 years, especially in the countries such as the UK that are staring from a position of historical high reliance on landfill. It is inevitable that we will see further consolidation of the market and that investors from a whole range of backgrounds will continue to be drawn to this sustainable growth market.

By John Raspin, Practice Director, Energy & Environment.

html>This article appears in the emagazine Earthtoys.