United States Sees 45V Tax Credit Clearing The Way For Clean Hydrogen, But Barriers Remain

The Biden administration has placed some big bets on clean hydrogen, seeing it as a replacement fuel for some hard-to-abate industries and putting it at the heart of its long-term decarbonization efforts. But while clean hydrogen has significant long-term potential — backed by major subsidies, including the 45V production tax credit (PTC) — figuring out a path to a greater role in the U.S. energy mix is more complicated than it might seem. The proposed rules around the tax credit have stirred up a hornet’s nest worth of criticism from those who think the guidance might ultimately do more harm than good. In today’s RBN blog, we’ll preview our latest Drill Down Report on the incentives — primarily the 45V tax credit — intended to expand the clean hydrogen industry and examine some of the barriers to significant growth.

Development of a clean-energy economy was a key plank in President Biden’s campaign platform four years ago and it has remained a priority since he took office in January 2021. With a focus on the short-term changes necessary to make any long-term goals viable, Biden set out some ambitious 2030 targets: at least 80% of U.S. power generated by renewable sources, a 50%-52% reduction (from 2005 levels) in greenhouse gas (GHG) emissions, and production of 10 million metric tons per annum (MMtpa) of clean hydrogen (ramping up to 20 MMtpa by 2040 and 50 MMtpa by 2050).

The administration was able to steer passage of two important pieces of legislation in its first two years: the Infrastructure Investment and Jobs Act (IIJA, better known as the Bipartisan Infrastructure Law) was passed in November 2021 and the Inflation Reduction Act (IRA) became law in August 2022. Among other things, the IIJA established $8 billion in federal funding for the development of a clean-hydrogen industry, including $7 billion for a series of regional hubs (see The Contenders for more) to be developed across the country. The IRA, widely seen as a game-changer regarding incentives around clean energy, includes provisions on everything from methane emissions and electric vehicles (EVs) to carbon capture and sequestration (CCS) and alternative fuels, but one of the most significant elements was the inclusion of the 45V tax credit.

Passage of the IRA set off intense debate (and lobbying) about how the guidelines around the 45V tax credit would be written and implemented. While some industry groups argued for looser guidelines around the PTC that would allow the clean hydrogen industry to grow quickly, others called for a stricter set of rules from the start, arguing that an approach that was too lax would fail in the ultimate goal to substantially decrease GHG emissions. Those guidelines were widely expected to be announced by August 2023, but as summer turned into fall, and fall into winter, it was clear that the debates over 45V were continuing inside the Biden administration. The rules were finally rolled out in December. Publication of the proposed rulemaking began a 60-day comment period, which concluded February 26.

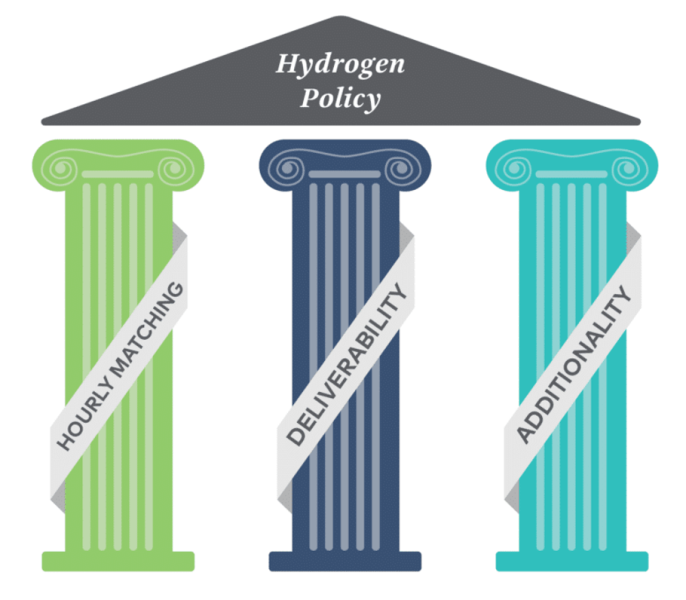

Figure 1. The “Three Pillars” of Clean Hydrogen Production. Source: 3Degrees

The proposed guidance relies on the use of energy attribute certificates (EACs) to demonstrate a hydrogen producer’s purchase of clean power. EACs are issued as proof of electricity produced by renewable sources. Each EAC verifies that 1 megawatt-hour (MWh) of electricity used by an electrolyzer was generated by 1 MWh generated from a renewable source, typically wind or solar. As illustrated in Figure 1 above, the guidelines establish the critical criteria — often referred to as the “three pillars” of clean hydrogen — that must be reflected in the EACs needed to claim the tax credit:

- Temporal matching, the focus of Section 2 of this report, requires electrolyzers’ electric consumption to match clean energy production over a set time frame (i.e., annual, monthly or hourly).

- Deliverability (Section 3) requires electrolyzers to source clean electricity from within their same operating region.

- Additionality (Section 4) requires the electricity for hydrogen production to come from new clean generation sources or an increase in the rate of electricity production from existing clean generation (known as uprating).

While the implementation of each of the “three pillars” comes with its own set of challenges, clean hydrogen faces plenty of other barriers to wider adoption. The biggest wild card, at least in the short term, is political, starting with the rules around 45V implementation, which will significantly affect the industry’s growth potential in the medium to long term. As noted above, the Biden administration took more than a year to come up with the proposed rulemaking around the tax credit, which has received a lot of criticism from industry groups and others that find it too restrictive, potentially stifling projects right from the start. There were nearly 400 comments about the proposed rulemaking submitted by corporations or organizations, an indication of how invested people are in the idea of clean hydrogen and its potential to be a game changer. Section 5 of our new report details some of the possible changes to the guidance around temporal matching, deliverability, and additionality that could be included in the final rulemaking, which is expected later this year. Other suggestions include the need to provide an early-mover advantage for the first group of projects to begin production and a call to incentivize all types of clean hydrogen since the current rulemaking strongly favors green hydrogen. (For more on the widely used — but occasionally scorned — hydrogen color scheme, see Don’t Let Me Be Misunderstood.)

This year’s debate over 45V could be dramatically overshadowed by other political considerations not too far down the road. With a Biden-Trump rematch set for November, the future of the nation’s energy policy — and the incentives that support several clean-energy initiatives — will be among the major issues up for debate. While President Biden would likely seek additional ways to reach his 2030 targets for clean hydrogen production and other goals, former President Trump has made no secret of his dislike for many portions of the IRA — the incentives for EVs and wind power seem to be popular targets — which adds at least some uncertainty to any long-term planning that centers on tax credits. If Trump were to be returned to office next year, the question of what happens to the IRA might be determined in large part by which party controls Congress. (Republicans currently hold a razor-thin advantage in the House, while 48 Democrats and three Democratic-leaning Independents hold a 51-49 margin in the Senate, where Vice President Harris can also provide a tie-breaking vote.)

None of the grand plans for hydrogen will come through — regardless of what happens to the federal incentives, this year or down the road — without the ability to get the necessary projects through the permitting process, an increasingly difficult task. As we noted in our Don’t Pass Me By series, almost everyone acknowledges the benefit of having interested parties and stakeholders weigh in on major proposals to build or expand infrastructure. Additionally, credible regulations and appropriate safeguards (such as the Clean Water Act’s focus on protecting the nation’s water supplies) are essential to the process. Still, the reality is that the permitting process for some important, badly needed projects — such as the transmission lines needed to power electrolyzers producing green hydrogen — can drag on for three, six, or even nine years or longer. Permitting delays not only drive up project costs but also put additional stress on infrastructure that’s already in place and prevents some projects from ever becoming a reality, putting a premium on the need for permitting reform at the federal level. But it’s important to note that opposition to wind and solar projects — again, essential elements of every plan to produce green hydrogen at scale — are increasingly being felt at the state and local levels.

Another unknown is whether a sufficient end-use market will develop to support all the additional clean hydrogen production that is supposed to come online down the road. Of the $8 billion in federal funding set aside to advance the industry, $1 billion is to support end-user demand. The initiative is intended to provide multi-year support for clean hydrogen produced by projects affiliated with the regional hubs. If it works as hoped, it would facilitate demand for clean hydrogen from a diverse set of off-takers across various sectors of the economy, including hard-to-abate industrial processes, manufacturing, and heavy-duty transportation. However the market will need a lot more than one incentive program to significantly scale up end-user demand, and it remains to be seen how soon green hydrogen (and other varieties) might be cost-competitive with gray hydrogen, the most common type produced.

One of the challenges to replacing gray hydrogen’s use in certain industries is the ability to store and transport clean hydrogen at an industrial scale. As we noted recently in our weekly Hydrogen Billboard, the development of a transportation and storage network is key to securing the offtake commitments critical to long-term growth. While there are several different ways to store hydrogen — including salt domes, above-ground tanks, depleted fields and aquifers, and hard-rock caverns — each comes with its own set of limitations. In addition, few of the announced hydrogen projects in the U.S. explicitly include plans for hydrogen storage. Backers of clean hydrogen see the eventual development of a nationwide pipeline network, but that’s a long way off. The U.S. currently has about 1,600 miles of hydrogen pipelines, almost entirely located in Texas and Louisiana where many large industrial users — such as refineries and petrochemical plants — are located (see our Hydrogen Infrastructure Map). By comparison, there are about 2.5 million miles of natural gas distribution lines in the U.S., according to the DOE.

We’ll continue to follow developments around the 45V rulemaking, the progress of clean hydrogen projects, and the often-fickle political winds that have the potential to shape them both.

For more information about the new Drill Down Report, click here » GO.

You can return to the main Market News page, or press the Back button on your browser.