Pot Holes Ahead for Global Tire Makers

Rising materials costs and heavy benefit burdens are giving the rubber barons a bumpy ride

The $70 billion global tire market is dominated by a few large players whose strong brand names and market positions have so far helped them weather major industry difficulties such as rising raw-material costs and the increasing burden of employee benefit costs. In 2006, however, they will find it more difficult to counter these trends as they have in the past with productivity gains, pricing improvements, and cost cutting.

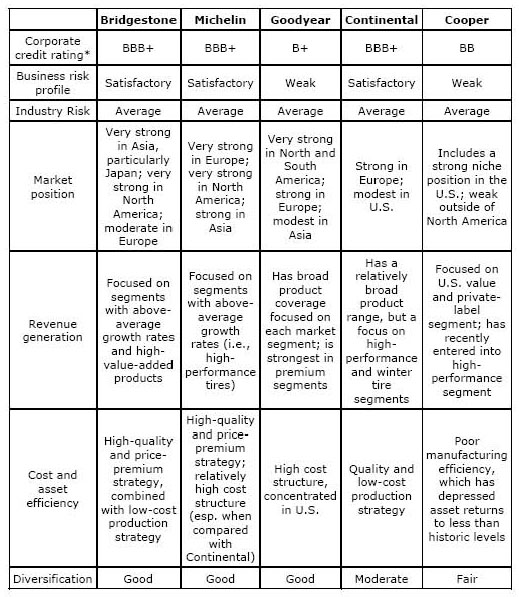

The major global players are Japan-based Bridgestone (S&P credit rating, BBB+), France-based Compagnie Generale des Etablissements Michelin (BBB+), U.S.-based Goodyear Tire & Rubber (B+), Germany-based Continental (BBB+), and U.S.-based Cooper Tire & Rubber (BB).

Currently, the top three manufacturers – Michelin, Bridgestone, and Goodyear (GT) – together command about 55% of the global market. There have been no meaningful changes in market-share movements in recent years, and we don’t expect any in the near future. All three players hold the leading market shares in their home continents, and somewhat weaker (but still meaningful) shares overseas. This global reach distinguishes them from their smaller competitors, Continental and Cooper Tire.

WARNING SIGNS

Standard & Poor’s Ratings Services believes the tire industry has an average industry risk profile, which is supported by the strong market positioning and broad distribution of the top-tier companies. All five tire manufacturers benefit from solid market positions in their main markets and regions, stakes that strongly support their ratings. Nevertheless, companies in this sector face numerous challenges, including:

For more information on Klean Industries Inc wholly own subsidiary, Mobius Enviro-Solutions Inc. - the world’s only integrated tire manufacturing and commodity recovery processing system please feel free to contact us and view this new release, Klean Industries unveils plans for revolutionary integrated tire manufacturing and pyrolysis recovery plant.

MATERIAL DAMAGE

In 2005, most of these rated peers have been able to confront such difficulties because they enjoyed healthy demand for consumer and commercial truck tires. Tire companies have also been mostly successful in their efforts to increase prices, improve their product mixes, and curtail costs.

The one exception is Cooper Tire, which saw its ratings fall from investment grade to speculative grade last year. The company is the smallest of the five and focuses on the U.S. replacement market. It has suffered from very poor operating performance during the past two years due to manufacturing inefficiencies, market-share losses, and labor disruptions.

WHAT ABOUT 2006?

Raw-material cost increases, which may not be adequately covered by future tire-price increases, continue to be the biggest risk for tire makers’ margins, cash-flow generation, and credit quality. Consequently, the combination of the overall flat volume of tires sold to original equipment (OE) manufacturers and rising raw-material and employee benefit costs remain the major near-term challenges in the industry. Aftermarket demand – which represents the largest proportion of total tire revenues – was mostly favorable in 2005, although demand has slowed so far in 2006.

REPLACEMENT DEMAND

The outlook for 2006 is for flat or decreasing OE tire sales in North America, flat or somewhat lower OE sales in Europe, flat or modest growth in global aftermarket demand, and continued strength in commercial-vehicle markets. Although tire makers were mostly able to counter adverse raw-material trends with productivity gains, pricing improvements, and cost-cutting efforts in 2005, this looks as if it will be much more challenging in 2006. Their flexibility to cope with demand fluctuations, and their pricing power to offset increasing costs, will be important credit considerations.

Europe, North America, and Asia have about equal shares of the global tire market. The market is dominated by the replacement segment, which accounts for 70% of units sold and 75% of sales revenue. This is a positive factor, as the replacement market is generally considered more stable than car and truck OE production, which has more volatile cycles.

In addition, customers in the replacement market are less price-sensitive and have less purchasing leverage than those in the OE market, though the tires in this segment are still considered price competitive. Market leaders Michelin, Goodyear, and Bridgestone tend to be the price leaders in their key markets.

COMING TOGETHER

Increased economic and social advancement in developing countries such as India and China will lead to the greater need for road transportation and thus greater tire volume. As overall tire demand grows with the total number of vehicles in use, this should spur growth in the replacement market.

Since 2000, there have been no large-scale mergers or acquisitions, partly because there are capital constraints on the leading players. Tire companies are also increasingly focused on internal operations in order to confront the difficult operating environment of the past few years.

Nevertheless, we believe that further consolidation is likely in the medium or longer term, and all of these rated companies except Goodyear are well positioned to play major roles in the process. Goodyear should be able to participate in the long term, although its heavy debt load will keep it from making meaningful financial investments for the time being.

Global Tire Makers: Business Risk Comparison

As of Mar. 15, 2006.

AGGRESSIVE CAPITAL

The three BBB+ rated companies (Bridgestone, Michelin, and Continental) have the highest tire-related EBITDA margins, amounting to about 13% to 16%, which ranks them clearly ahead of the 7% to 10% EBITDA margins of Goodyear and Cooper Tire. Four of the companies (all but Cooper Tire) sustained or improved profit margins in 2005 because of price increases, mix improvements, and/or higher capacity utilization, which offset significantly higher raw-material costs.

Goodyear’s margins have also been helped by extensive restructuring actions, including the closure of a high-cost manufacturing facility in the U.S., and by various corporate overhead personnel reductions. Cooper Tire’s EBITDA margins have fallen significantly in the past few years, to 7% in 2005 from 13% in 2002.

Most of the major tire manufacturers have fairly aggressive capital structures, although they have reduced some debt in recent years. High leverage is partly due to significant unfunded post-employment benefit obligations, which are typical of the industry. Companies with a strong balance sheet could have a competitive advantage over those with heavy debt loads, since they can respond quickly to growth opportunities and meet hefty investment requirements.

MAKING THE GRADE

As Standard & Poor’s treats unfunded postemployment pension and medical liabilities as debt-like, any increase in such obligations further harms the capital structure in our assessment. Rated tire makers have all seen the net present value of their underfunded benefit liabilities increase during the past five years because of lower discount rates, weak plan-asset returns, and high growth rates for health-care costs.

These obligations, with their annual service and interest costs, are a substantial burden for the tire makers. Goodyear, for one, is saddled with massive benefit exposures that account for 46% of the company’s total liabilities.

S&P considers Michelin, Bridgestone, and Continental to have the strongest liquidity and financial flexibility, which helps buttress their investment-grade ratings. Michelin still has good liquidity, derived from its available cash and credit lines, though this liquidity has weakened in the past year. Bridgestone’s and Continental’s good liquidity stems from solid free cash flow generation.

Cooper Tire has good liquidity because of its excess cash balances, unused bank lines, and limited near-term debt maturities. Goodyear’s liquidity and financial flexibility are adequate in the near term because of the company’s healthy cash balances and access to credit facilities. In the medium term, however, the company must contend with a highly leveraged capital structure and burdensome pension funding requirements.

From Standard & Poor’s Ratings Services

All of the views expressed in this research report accurately reflect the research analyst’s personal views regarding any and all of the subject securities or issuers. No part of analyst compensation was, is or will be, directly or indirectly related to the specific recommendations or views expressed in this research report.

“Standard & Poor’s Regulatory Disclosure”

Any advice, analysis, or recommendations contained in articles labeled “Insight from Standard & Poor’s” reflect the views of Standard & Poor’s, which operates separately from and independently of BusinessWeek Online. It is possible that BWOL may from time to time publish information that is not consistent with advice, analysis, or recommendations that are published by Standard & Poor’s. Standard & Poor’s and BusinessWeek Online are each units of The McGraw-Hill Companies, Inc.

For further information please read the following press release click here and contact:

Mr. Marc Smith

#525 - 999 West Hastings St.

Vancouver, B.C.,

Canada, V6E 2W2

Tel: +1.604.408.0357

Fax: +1.604.730.8557

The $70 billion global tire market is dominated by a few large players whose strong brand names and market positions have so far helped them weather major industry difficulties such as rising raw-material costs and the increasing burden of employee benefit costs. In 2006, however, they will find it more difficult to counter these trends as they have in the past with productivity gains, pricing improvements, and cost cutting.

The major global players are Japan-based Bridgestone (S&P credit rating, BBB+), France-based Compagnie Generale des Etablissements Michelin (BBB+), U.S.-based Goodyear Tire & Rubber (B+), Germany-based Continental (BBB+), and U.S.-based Cooper Tire & Rubber (BB).

Currently, the top three manufacturers – Michelin, Bridgestone, and Goodyear (GT) – together command about 55% of the global market. There have been no meaningful changes in market-share movements in recent years, and we don’t expect any in the near future. All three players hold the leading market shares in their home continents, and somewhat weaker (but still meaningful) shares overseas. This global reach distinguishes them from their smaller competitors, Continental and Cooper Tire.

WARNING SIGNS

Standard & Poor’s Ratings Services believes the tire industry has an average industry risk profile, which is supported by the strong market positioning and broad distribution of the top-tier companies. All five tire manufacturers benefit from solid market positions in their main markets and regions, stakes that strongly support their ratings. Nevertheless, companies in this sector face numerous challenges, including:

- Uncertainty about auto production volumes over the next few years;

- Restrained consumer spending owing to uncertain economic conditions and fragile consumer confidence;

- Increasing competition, as niche players expand their product lines and geographic presence;

- High capital expenditures and R&D costs, which are necessary to support new product development and productivity-improvement initiatives;

- The need to lay out high labor and employee-benefit costs in high-volume markets;

- Volatile raw-material and energy costs;

- Exposure to foreign-exchange movements; and

- The need to expand into underdeveloped, high-growth markets.

For more information on Klean Industries Inc wholly own subsidiary, Mobius Enviro-Solutions Inc. - the world’s only integrated tire manufacturing and commodity recovery processing system please feel free to contact us and view this new release, Klean Industries unveils plans for revolutionary integrated tire manufacturing and pyrolysis recovery plant.

MATERIAL DAMAGE

In 2005, most of these rated peers have been able to confront such difficulties because they enjoyed healthy demand for consumer and commercial truck tires. Tire companies have also been mostly successful in their efforts to increase prices, improve their product mixes, and curtail costs.

The one exception is Cooper Tire, which saw its ratings fall from investment grade to speculative grade last year. The company is the smallest of the five and focuses on the U.S. replacement market. It has suffered from very poor operating performance during the past two years due to manufacturing inefficiencies, market-share losses, and labor disruptions.

WHAT ABOUT 2006?

Raw-material cost increases, which may not be adequately covered by future tire-price increases, continue to be the biggest risk for tire makers’ margins, cash-flow generation, and credit quality. Consequently, the combination of the overall flat volume of tires sold to original equipment (OE) manufacturers and rising raw-material and employee benefit costs remain the major near-term challenges in the industry. Aftermarket demand – which represents the largest proportion of total tire revenues – was mostly favorable in 2005, although demand has slowed so far in 2006.

REPLACEMENT DEMAND

The outlook for 2006 is for flat or decreasing OE tire sales in North America, flat or somewhat lower OE sales in Europe, flat or modest growth in global aftermarket demand, and continued strength in commercial-vehicle markets. Although tire makers were mostly able to counter adverse raw-material trends with productivity gains, pricing improvements, and cost-cutting efforts in 2005, this looks as if it will be much more challenging in 2006. Their flexibility to cope with demand fluctuations, and their pricing power to offset increasing costs, will be important credit considerations.

Europe, North America, and Asia have about equal shares of the global tire market. The market is dominated by the replacement segment, which accounts for 70% of units sold and 75% of sales revenue. This is a positive factor, as the replacement market is generally considered more stable than car and truck OE production, which has more volatile cycles.

In addition, customers in the replacement market are less price-sensitive and have less purchasing leverage than those in the OE market, though the tires in this segment are still considered price competitive. Market leaders Michelin, Goodyear, and Bridgestone tend to be the price leaders in their key markets.

COMING TOGETHER

Increased economic and social advancement in developing countries such as India and China will lead to the greater need for road transportation and thus greater tire volume. As overall tire demand grows with the total number of vehicles in use, this should spur growth in the replacement market.

Since 2000, there have been no large-scale mergers or acquisitions, partly because there are capital constraints on the leading players. Tire companies are also increasingly focused on internal operations in order to confront the difficult operating environment of the past few years.

Nevertheless, we believe that further consolidation is likely in the medium or longer term, and all of these rated companies except Goodyear are well positioned to play major roles in the process. Goodyear should be able to participate in the long term, although its heavy debt load will keep it from making meaningful financial investments for the time being.

Global Tire Makers: Business Risk Comparison

As of Mar. 15, 2006.

AGGRESSIVE CAPITAL

The three BBB+ rated companies (Bridgestone, Michelin, and Continental) have the highest tire-related EBITDA margins, amounting to about 13% to 16%, which ranks them clearly ahead of the 7% to 10% EBITDA margins of Goodyear and Cooper Tire. Four of the companies (all but Cooper Tire) sustained or improved profit margins in 2005 because of price increases, mix improvements, and/or higher capacity utilization, which offset significantly higher raw-material costs.

Goodyear’s margins have also been helped by extensive restructuring actions, including the closure of a high-cost manufacturing facility in the U.S., and by various corporate overhead personnel reductions. Cooper Tire’s EBITDA margins have fallen significantly in the past few years, to 7% in 2005 from 13% in 2002.

Most of the major tire manufacturers have fairly aggressive capital structures, although they have reduced some debt in recent years. High leverage is partly due to significant unfunded post-employment benefit obligations, which are typical of the industry. Companies with a strong balance sheet could have a competitive advantage over those with heavy debt loads, since they can respond quickly to growth opportunities and meet hefty investment requirements.

MAKING THE GRADE

As Standard & Poor’s treats unfunded postemployment pension and medical liabilities as debt-like, any increase in such obligations further harms the capital structure in our assessment. Rated tire makers have all seen the net present value of their underfunded benefit liabilities increase during the past five years because of lower discount rates, weak plan-asset returns, and high growth rates for health-care costs.

These obligations, with their annual service and interest costs, are a substantial burden for the tire makers. Goodyear, for one, is saddled with massive benefit exposures that account for 46% of the company’s total liabilities.

S&P considers Michelin, Bridgestone, and Continental to have the strongest liquidity and financial flexibility, which helps buttress their investment-grade ratings. Michelin still has good liquidity, derived from its available cash and credit lines, though this liquidity has weakened in the past year. Bridgestone’s and Continental’s good liquidity stems from solid free cash flow generation.

Cooper Tire has good liquidity because of its excess cash balances, unused bank lines, and limited near-term debt maturities. Goodyear’s liquidity and financial flexibility are adequate in the near term because of the company’s healthy cash balances and access to credit facilities. In the medium term, however, the company must contend with a highly leveraged capital structure and burdensome pension funding requirements.

From Standard & Poor’s Ratings Services

All of the views expressed in this research report accurately reflect the research analyst’s personal views regarding any and all of the subject securities or issuers. No part of analyst compensation was, is or will be, directly or indirectly related to the specific recommendations or views expressed in this research report.

“Standard & Poor’s Regulatory Disclosure”

Any advice, analysis, or recommendations contained in articles labeled “Insight from Standard & Poor’s” reflect the views of Standard & Poor’s, which operates separately from and independently of BusinessWeek Online. It is possible that BWOL may from time to time publish information that is not consistent with advice, analysis, or recommendations that are published by Standard & Poor’s. Standard & Poor’s and BusinessWeek Online are each units of The McGraw-Hill Companies, Inc.

For further information please read the following press release click here and contact:

Mr. Marc Smith

#525 - 999 West Hastings St.

Vancouver, B.C.,

Canada, V6E 2W2

Tel: +1.604.408.0357

Fax: +1.604.730.8557

You can return to the main Market News page, or press the Back button on your browser.