Leadership lessons for hard times

During the current global recession, much attention has been devoted to the mistakes that sparked the financial and economic crisis, in hopes of not repeating them. Less has been given to what’s been done well amid the turmoil—to learn, for example, how best to lead a company through these tough times.

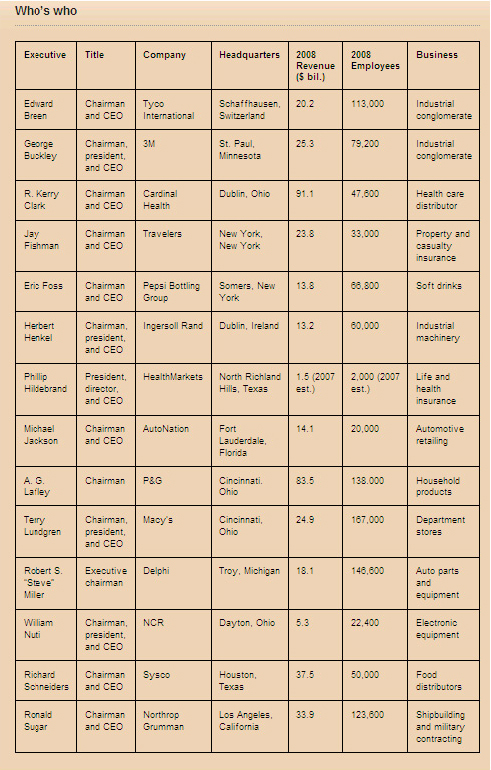

To contribute to that understanding, we interviewed the leaders of 14 major companies (see sidebar, “Who’s who”), all seasoned CEOs or chairmen, asking them to reflect on what they felt they had learned. We were keen not to limit their comments to the current recession and therefore also asked them to consider previous challenges they had faced in a turnaround or a crisis. The companies they lead are in different industries, face different challenges, and have performed quite differently. We are attempting neither to judge their performance nor to draw up a set of rules on how to lead through tough times. Instead, what emerges from the interviews is agreement on some broad principles that can help guide behavior in the executive suite and the boardroom, as well as interactions with employees, customers, and investors.

Confront reality

Always question whether the “halo effect” of a business or business situation is blinding you to what lies on the horizon.—Herbert Henkel, chairman and CEO of Ingersoll Rand

Few predicted the magnitude of the current crisis. But those in the corporate world who first detected—and accepted—the fact that something was amiss had a distinct advantage in implementing strategies to help weather the storm.

In the summer of 2008, Ingersoll Rand’s Herbert Henkel noticed that European orders in the company’s transport refrigeration business had slumped, even though business was still booming in other divisions. He was alarmed: a fall in the delivery of perishable foods surely indicated trouble in the supply chain. “I couldn’t help thinking, what if that figure really is indicative of what’s out ahead? What are we going to do about it?”

Henkel, squaring up to what he detected, forecast zero growth in Europe during the third quarter, though analysts thought he was “nuts.” His forecast was wrong: growth fell by 15 percent. Yet Ingersoll Rand got ahead of the curve by quickly putting contingency plans in place, restructuring, and running down inventory. “Of course, we still had to go back and do more. But by not ignoring that one indicator, we did get a head start,” he reflects.

Getting ahead of the curve means taking a hard look at what the future might hold, and that requires a degree of courage. The point made by Henkel and others is how difficult it can be for leaders to take action—and to persuade others to follow their lead—if a business seems to be thriving.

Eight years ago, when Michael Jackson arrived at AutoNation, for example, the auto industry was selling as many as 17 million units a year, but its high fixed costs made him fear what would happen if the economic environment changed. At his first management meeting, he therefore announced his desire to find a business model that would let AutoNation break even if the auto industry sold only 10 million units. He also wanted to understand what would have to happen for sales to take such a nosedive and how the business would need to be remodeled to survive. “Everybody looked at me like I had six heads,” he recalls. “Eventually, we came to the conclusion that, among other things, it would take a credit crisis to get volumes that low, because in our business, nothing moves without credit. So we got out of the finance and leasing business,” says Jackson. “Without the limitation on risk we put in place, we would be in deep, serious trouble at the moment.”

CEOs also need courage to make hard decisions quickly. Phil Hildebrand, of HealthMarkets, and Steve Miller, of Delphi, both remarked on the importance of decisiveness to prevent problems from escalating. But it can be hard to achieve in the absence of perfect data. “A lot of CEOs are slow to react, and their problems get away from them,” says Edward Breen, of Tyco International. “You have to get as much data as quickly as possible. But you will never get all of it—so you need to make decisions quickly.”

Besides courage, staying ahead of the curve entails having the mechanisms and governance models that allow companies to confront realities unimaginably different from those they would ordinarily expect. Monitoring systems that pick up warning signs are important. So too is an environment, both physical and psychological, where alternative interpretations of the signs can be aired and considered with care and interest.

At Cardinal Health, Kerry Clark wanted to have a better grasp of such potentially unpleasant realities and felt that historical practice—employees were given forecasts and simply told to meet them—was a hindrance. Instead, he made business leaders accountable for making forecasts and doing everything possible to meet them, while regularly and openly reviewing them. “It’s all too easy for a corporate leader to say, ‘Don’t give me more bad news. Just go fix it,’” muses Clark. “But you have to beat back that kind of attitude and create an atmosphere where people feel they can talk about the forecast, how they can improve it, and what resources they might need.” He says that the new system required a cultural change but is yielding results—for instance, revealing problems earlier.

Sysco’s Richard Schneiders puts it this way: “You have to be open to diverse points of view. Given the speed of change, I don’t know how a business will be able to continue to flourish in the future without being receptive to different points of view.”

At board meetings, put strategy center stage

The board has been heavily involved in strategy formulation with me, and we have a better strategy because of it.—Bill Nuti, chairman and CEO of NCR

The way CEOs work with their boards has changed fundamentally during the past year. In tough times, difficult decisions must be made quickly, so it’s not surprising that many CEO find themselves communicating more regularly with the board to keep it abreast of developments. Full board meetings have been supplemented by letters, e-mails, intranet postings, informal discussions, and conference calls. At Cardinal Health, “board updates”—conference calls held as frequently as every two weeks—address questions from board members. “They weren’t board meetings. There were no minutes. No one was obliged to attend. But it was very helpful,” says Clark, who sees the updates as an efficient way to address individual concerns and increase confidence in the management team.

Many CEOs have already accepted the need for frequent and open communication with their boards, a practice they say proves its worth when difficult decisions must be made. If directors are up to speed, they are better placed to offer both support and advice. What has changed markedly is the content of board discussions. In particular, discussions about strategy are no longer the preserve of a once-a-year off-site meeting. The pace of change—crisis or no crisis—makes that model unworkable.

Today, at many companies, strategy is on the agenda of every board meeting. “The world moves at a pace that requires strategy to be front and center all of the time,” says NCR’s Bill Nuti. “There are too many variables that come into play in a normal cycle, let alone this one, that can rapidly change the course of your company, so I bring strategy up at every single meeting.” Eric Foss, of Pepsi Bottling, decided to integrate strategy into every board meeting at the beginning of 2008, before the crisis. It was a fortunate decision, according to Foss, considering the board’s contribution. He, like others, is happy to communicate more frequently with a talented board not just to build its trust but also to benefit from its experience. Several CEOs said that working to get the right people with the right experience onto their boards had been a priority, over the course of several years, for that very reason.

Nuti credits his board with helping him understand the potential magnitude of the current downturn very quickly. “You get great research when you can pull information from board members who all sit on 2 or 3 boards. You’re getting the perspective of 18 different boards. I was looking for commonality in their feedback and, fortunately—or unfortunately, in the light of circumstances—there was a lot of commonality.”

Be transparent with employees …

The only way to address uncertainty is to communicate and communicate. And when you think you’ve just about got to everybody, then communicate some more.—Terry Lundgren, chairman, president, and CEO of Macy’s

One legacy of the current downturn will be a reinforced belief in the value of frequent, transparent communication with employees, and not just the CEO’s direct reports. The CEOs we interviewed could not overemphasize the power of openness at all levels.

“At Cardinal, we work hard on internal communications,” says Clark. “We do a lot of town hall meetings, for example. We used to just do them around earnings time, but now we do them to discuss any major initiative that’s under way.” Clark also notes that investor relations (IR) and internal communications work hand in hand, so that any information that goes to the investor community is reworked for employees. “We do a very good job of making sure information doesn’t get in front of one group without getting in front of the other.”

Being open about what is happening in a company is partly a question of integrity: employees deserve honesty. Openness also builds respect, trust, and solidarity, all of which in turn help employees stay focused on the task of running the business at a time when financial rewards might be limited and the future uncertain. Openness helps build morale as well. A CEO cannot mislead people and certainly shouldn’t panic them, but explaining problems and the actions being taken to deal with them builds confidence in the quality of the CEO’s leadership. “People will take any hill, walk into the worst situation, if they have faith in your leadership and know what your strategy and objectives are,” says Tyco’s Breen.

3M’s George Buckley emphasizes, in addition, the need to assure employees that the CEO has faith in them and that they will not be blamed for things beyond their control—such as the state of the economy. “When they’re battling the marketplace, they need to know you will support them,” he says.

Finally, openness helps ensure that everyone in an organization understands how to make a difference. When the CEO explains “the current situation,” says Ingersoll Rand’s Henkel, “people understand why we need cash both to pay off debt and to be able to continue making investments. That, for example, makes them think twice about ordering something just to be on the safe side.”

Yet although the importance of good internal communication is widely understood, it can slip from the priority list in a crisis. “In hard times, we ask employees to work harder than ever,” comments P&G’s A. G. Lafley. “But in hard times, you get caught up with investors, analysts, the media, suppliers, and retailers. It’s all too easy to overlook your employees at precisely the time you should be communicating more with them.”

… and investors

Our policy is: “If in doubt, communicate.” We always want to conduct our business with integrity and forthrightness.—Ron Sugar, chairman and CEO of Northrop Grumman

Most CEOs we interviewed have noticed that the amount of time they spend communicating with investors has risen exponentially of late. Here too they strive to be as open as possible. “If I’ve learned anything in the last 18 months, it’s that transparency in troubled times really matters,” says Travelers’ Jay Fishman. Yet he believes the crisis has revealed that transparency still goes against the grain for many people. “If asked to describe this or that exposure, the advice from many IR departments is to use some formulation that basically says don’t worry. I’ve tried to resist that. Now is not the time to tell people not to worry. If you’re in the financial-services industry, you ought to be able to quantify. I try to be specific, and we’ve gained credibility as a result.” Pepsi’s Foss too recommends transparency with investors: “we’re facing up to our issues” and in this way “demonstrating that we have a management team that knows what it’s doing.”

But there are caveats. In times of crisis, there can be a tendency to focus entirely on short-term results—a tendency CEOs should counter. While acknowledging current difficulties, it is just as important to emphasize what is being done to build a company’s longer-term health. Fishman, like others, has spent much time talking about his company’s mid- and long-term strategy, its efforts to improve productivity, and his willingness to sacrifice some short-term performance to create longer-term value.

There is also a feeling among CEOs that not all investors are equal. While chief executives are acutely aware of disclosure requirements, some say that their companies would gain very little if they spent more time with short-term investors. CEOs count themselves lucky when they feel strategically aligned with long-term investors who have large holdings. That makes these CEOs believe they have some breathing space in a crisis, and as a result they may not have to spend a great deal more time with their investors. But they note how hard they worked to recruit those investors.

When Jackson took over at AutoNation, for instance, he knew that to succeed he would have to attract a new shareholder base prepared to sacrifice some short-term profit for longer-term gain. “The investors I have now understand the business model, and that’s been a huge plus. But it didn’t happen by itself,” he points out.

Build and protect the culture

Stay focused on culture, people, and values: it’s the area most likely to get compromised in this environment.—Eric Foss, chairman and CEO of Pepsi Bottling Group

A healthy company enjoys not only strong financials but also a culture and values that bind it together. Much of what our interviewees describe as important is driven by corporate culture—open communication or a focus on a company’s long-term health, for example. Several CEOs chose to highlight how a strong culture had helped them in hard times and how important it is not to sacrifice that culture when a company comes under pressure.

Jackson says that the most critical battle he waged when he arrived at AutoNation was destroying the “growth at any cost” culture. “We wanted entrepreneurialism, but we also wanted the highest standards of integrity.” Over the next three years, he worked hard to nurture and recruit the right people for the company’s top 350 positions and to purge the “high-performing money makers whose risk profile would keep you awake at night.” This amounted, he says, to a cultural revolution that has delivered a sustainable competitive advantage—and one that he isn’t about to jeopardize by shedding his best talent.

Lafley too feels that the culture he worked hard to build at the beginning of the decade at P&G has paid off. Concerned that the company had become too inward looking, he flipped that around. “Take trust. We only ever talked about it in relation to employees. But what matters most now is that consumers trust our brand, that shareholders trust our stock, that customers trust us to be the best supplier, and that suppliers trust us to be their best customer.”

At Travelers, Fishman is proud of the culture he has nurtured, which rewards returns on capital rather than revenue and has offered some protection during the financial crisis. “We never criticize anyone for a transaction not done, not ever—not ever,” he says.

Keep faith with the future

If you don’t invest in the future and don’t plan for the future, there won’t be one.—George Buckley, chairman, president, and CEO of 3M

CEOs and their leadership teams need to remain forward looking despite the near-term pressures their businesses might be facing. There are opportunities in a crisis, even though that notion is too lightly bandied around when companies and their employees come under real stress. Many of the CEOs we interviewed were determined to ensure that their companies emerge from this recession with a competitive advantage by setting the course for higher productivity, acquiring a footprint in a new market, or not squandering a company’s talent or reputation in pursuit of lower costs.

Likewise, at P&G, Lafley continues to look for growth opportunities through alliances and acquisitions and is increasing the company’s investment in R&D and innovation. His efforts require resolve. “We’re keeping the pedal to the metal on innovation, for example, but it’s not always easy when people are complaining about your short-term profit performance. You have to get the balance right between the present and the future, but we want to come out of this recession stronger than we went in,” he declares.

Nuti too acknowledges the difficulty of looking to the future while concentrating on a challenging present. When he arrived at NCR, in 2005, he was concerned that although the company was rightly focused on cost cutting to regain profitability, it had no plan for the future. “My challenge, up to and including the last six to eight months, has been to keep driving the transformation of the company while still adapting to the realities of the present. You can’t cut the things that will impact your ability to reach your vision.” Nuti suggests using a scalpel rather than an ax. The ax will make the biggest dent on costs and make you look smart for a while. But the more precise scalpel can protect a company’s future, even if there are fewer short-term gains.

None of the CEOs we interviewed claimed to have attempted anything revolutionary. What was evident, however, was their resolve in pursuing the principles they thought were right, often in the face of opposition. Leadership becomes increasingly important in tough times, when so much is at risk—but it can be even harder to exercise. The six leadership “musts” described in this article have made the greatest difference for CEOs on the front line.

About the Authors

Michael Patsalos-Fox is a director in McKinsey’s New York office, Dennis Carey is a senior client partner of board and CEO recruiting at Korn/Ferry International, and Michael Useem is the William and Jacalyn Egan Professor of Management and the director of the Center for Leadership and Change Management at the Wharton School of the University of Pennsylvania.

You can return to the main Market News page, or press the Back button on your browser.