China's Wind Industry

Introduction

The international financial crisis, which has reverberated deeply into China’s economy, certainly has had an impact on the Chinese wind power sector in a number of ways. It has contributed to declining prices for certified emissions reduction credits (CERs) under the CDM Kyoto Protocol framework, a key subsidy for wind farm development, caused some foreign companies to exit the Chinese wind farm development business as oil prices have declined and credit has become more difficult to obtain and costly to acquire and brought on the recession that has resulted in declining energy use and falling power prices throughout China.

By most accounts, however, the impact of this worldwide financial upheaval has been limited with respect to China’s burgeoning wind power industry. In part this is attributable to the fact that the Chinese wind industry’s development is in large measure directed by Beijing and 80% of the market is concentrated in large state-owned enterprises. It is also due to the decision of the leadership in Beijing to forge ahead with renewable energy development as one element of its approach to combating the economic downturn China now faces. In fact, the centerpiece of Beijing’s response to the economic slowdown in China set off by the subprime mortgage breakdown is a $586 billion U.S. stimulus package, a quarter of which amount will be allocated to environmental, renewable energy and energy efficiency projects. Like the incoming Obama administration in the U.S., the Chinese government understands that they also can get a “two-fer” by funding renewable energy and energy efficiency projects that will both spur economic development and advance China towards its goal of a cleaner and more sustainable energy future (for every 1000 MW of wind power that is installed there is a reduction in carbon dioxide emissions of approximately 2.5 million tpy). So the silver lining in the clouds that darken the world’s economic landscape is that China appears more committed than ever to forge ahead with a robust program of renewable energy development, a key component of which is wind power development. That commitment already is being displayed; in the fourth quarter of 2008, of the 100 billion Yuan (~$14.8 billion U.S.D.) that the Chinese government is using to stimulate the economy through investment in renewable energy, a sizeable portion is being allocated to wind power projects.

Wind Power Will Be An Important Source of Power in China

While wind power in China now accounts for just 1.3% of total power output in China (compared with coal fired power at 75% of total power output), only three years ago wind power only accounted for 1/1000th of total power production in China. At the pace that installed capacity to produce power from the wind is being built in China, the contribution to total power needs from wind will continue to increase as the Chinese wind industry matures and the cost per Kwh to produce wind power continues to decrease. At the same time the restructuring of the power industry to reduce the number of small and disproportionately polluting coal-fired power plants will result in a more sustainable mix of power sources over time. China is making progress towards its plan to close a total of 50,000 MW of small, inefficient and highly polluting coal-fired power plants over the course of the 11th Five Year Plan Period (2006-2010); Beijing reports that through October 2008 it already has closed 32,100 MW of these offending power plants and plans to close an additional 13,000 MW of such small power plants in 2009. The process of rationalizing the coal-fired power plants in China is projected to save 40 million tpy of coal and reduce sulfur dioxide emissions and carbon dioxide emissions by, respectively, 680,000 tpy and 65 million tpy. Chinese planners envision a future mix of power generating sources totaling 1.2 million to 1.5 million MW (an average of 1KW/person/year), comprised on no more than 800,000 MW of coal-fired power plants, 200,000 to 300,000 MW of hydropower and wind power and 200,000 MW of nuclear energy.

The Accelerating Growth of Wind Power

China’s wind energy potential is enormous. Chinese sources estimate that exploitable “wind resources” that are available on land in China may be as high as 600,000 to 1 million MW and that close-in off-shore exploitable wind power potential accounts for another 700,000 MW. Since the {Renewable Energy Law} took effect on January 1, 2006, China’s installed capacity to produce wind power has increased from 2300 MW as of the end of 2005, to in excess of 3200 MW as of the end of 2006, to 5900 MW as of the end of 2007 to more than 7000 MW as of mid-year 2008. Through the end of 2007 China had built more than 100 wind farms in 22 provinces and cities. China is on track to reach the symbolically important milestone of 10,000 MW of installed wind power as of the end of 2008—two years ahead of the revised goal. By 2010 cumulative installed capacity to produce wind power may reach 15,000 to 20,000 MW and after 2011 China will be adding new capacity at the rate of 7000-10,000 MW/year. By 2015 analysts predict that China’s base of wind power installations will total 50,000 to 60,000 MW and that by 2020 wind power will account for 80,000-100,000 MW of power generation in China; the goal for 2020 was revised upward four-fold from the 30,000 MW goal set by the {Mid to Long Term Development Plan for Renewable Energy} promulgated by Beijing in September 2007. (See accompanying chart). Central to this rapid development of wind power capacity in China is a series of ambitious mega-wind farm projects. There already are a series of such projects that are in planning (and at least one under construction) that should result in a total of approximately 100,000 MW of wind power by 2020 among only six mega-projects! These six large wind farm “bases” include 12,000 MW in Gansu Province; 20,000 MW in Hami in Xinjiang Province; 20,000 MW in Western Inner Mongolia; 30,000 MW in Eastern Inner Mongolia; 10,000 MW in Hebei Province; and 10,000 MW in Jiangsu Province.

As the third fastest growing wind power market in the world (after the U.S. and Spain) and the fifth largest installed base of wind power, in 2007 China attracted 15% of the world’s investment in wind power. According to Mr. Li Junfeng, the Vice-Chairman of the Energy Institute of the National Development and Reform Commission, in 2007 alone, China’s wind industry attracted investments totaling 34 billion Yuan (~$5 billion U.S.D.).

China’s Wind Power Equipment Manufacturing Industry

After several years of development, China’s wind power equipment manufacturing industry has now achieved a certain scale of operations and technological competence that will certainly help accelerate the development of wind power in China in the years ahead. Even with its rapid growth, however, the Chinese wind power equipment manufacturing industry is not yet keeping pace with demand. According to Chinese sources, there are now sixty-seven wind turbine manufacturers operating in China (up from 40 in mid 2007 and only 6 in 2004), including 27 state-owned or state controlled companies; 23 private companies; 8 joint venture companies and 9 wholly foreign-owned companies. Chinese wind turbine manufacturers in 2007 for the first time accounted for more than 50% (55.4%) of all wind turbines installed in China and because Chinese wind turbine manufacturers are now capable of producing 1.5 MW, 2 MW and now even 3 MW wind turbines, the expectation is that Chinese companies’ share of wind turbine installations will continue to increase. Though the numbers of wind turbine manufacturers have increased, the most significant Chinese competitors are Xinjiang Goldwind (Jin Feng) Science and Technology Joint Stock Co., Ltd., Dongfang and Sinovel Wind Power Science and Technology Co., Ltd. In the view of Han Junliang, the Chairman of Sinovel, the financial crisis will benefit the Chinese wind industry by hastening the consolidation of the wind turbine manufacturers. The percentage of wind turbines that are sourced domestically will increase as a consequence of the {Notice Concerning Certain Requirements for Wind Farm Construction Management}, which requires that 70% of the equipment sourced for any wind farm project must be sourced domestically. Tariff changes also have had the effect of supporting the development of the domestic wind turbine industry. On April 23, 2008 the Ministry of Finance announced the elimination, as of May 1, 2008, of tariff free importation of wind turbines that are less than 2.5 MW (tariff classification $85023100).

As more than 80% of the cost of a wind turbine is in the parts, the relatively quick development of an indigenous wind power equipment parts industry also is a sign of increasing maturity. The indigenous industry producing gearboxes, generators and blades is able to satisfy current demand in China, though the fact that there are now more than fifty of such companies presages intensified competition and perhaps the gradual appearance of these products on the export market. China remains largely dependent on imports for such key components as precision bearings, electrical and control systems and inverters. American Superconductor Corp. (AMSC), for example, has been enormously successful in selling its electrical and control systems to Chinese wind turbine manufacturers, such as Sinovel. To facilitate the import of components that are not being manufactured in China, as of January 1, 2008, the Ministry of Finance instituted a program of rebates of tariffs and VAT taxes paid on the importation of parts and raw materials used in the manufacture of wind turbines.

The development of an indigenous manufacturing base to support the growth of wind power installations in China promises to achieve the cost reductions that will continue to drive down the cost of this alternative energy source. Presently the cost of wind power is 0.5-0.6 Yuan/Kwh; the cost of thermal power from coal-fired power plants presently is 0.2-0.3 Yuan/Kwh. While only 19% of the 6458 wind turbines that were installed in China as of the end of 2007 were indigenously produced MW-class wind turbines, the pace of adoption of domestic wind turbines is increasing and this will increasingly result in significant cost savings for the industry. According to the Chinese, if 70% of wind turbines are manufactured locally, the cost of wind turbines can be reduced by 15% and without any other changes in cost structure, the reduced cost of wind turbines can result in a reduction in power generation costs to 0.375 Yuan/Kwh. If all wind turbines are manufactured domestically, the cost of wind turbines will decline a total of 30% and, again without any other cost savings factored in, the power generation costs of wind will decline to 0.332 Yuan/Kwh. Factoring in a cost associated with the pollution caused by coal fired power plants and the likelihood that fossil fuel prices will increase, the Chinese believe that they can achieve pricing parity between coal-fired power and wind power in the foreseeable future. The Chinese recognize that to achieve the cost reductions that will enable the industry to become cost competitive with coal-fired power plants, it will be imperative for them to invest, on average, 1.5-3% of the cost of a wind farm on science and technology research and development. In the short term the wind turbine industry will benefit from the drop in prices for steel and other materials used in the manufacture of wind turbines. As Chinese wind turbine manufacturing improves, the stage will be set for Chinese wind turbine and components manufacturers also to begin to export to the world.

Foreign wind power equipment manufacturers, including Denmark’s Vestas, India’s Suzlon, Spain’s Gamesa, Germany’s Nordex Corp. and GE Energy, aggressively have engaged the Chinese wind market. The spate of new wind turbine plants that foreign wind turbine manufacturers are building in China is a result of the explosive growth in wind power capacity development in China, but also a result of Chinese industrial policy that penalizes foreign imports and rewards domestically produced wind turbines. At 60 million Euros, Gamesa’s factory in Tianjin, which manufacturers wind turbines, is the Spanish company’s second largest foreign investment (after the U.S.) Nordex has located two of its three manufacturing centers in China and has established the company’s Asia headquarters in Beijing. Nordex expects to invest an additional 500 million Yuan (~$71 million U.S.D.) and grow its business in China four-fold in the next three years. Though foreign wind turbine manufacturers have a cumulative market share (total installed base) of the Chinese wind power equipment market of 65.9%, the inroads made by the emerging domestic Chinese wind turbine industry are evident in the fact that the foreign manufacturers market share of current installations has declined to 55.1%. The industrial policies of the Chinese government with respect to the emerging Chinese wind power industry—policies that have been described as “escorting the Emperor”—are contributing to the decline in market share of foreign manufacturers. The ability of Chinese companies to move more swiftly than foreign competitors to build factories and secure sales in China also contributes to the erosion of market share by foreign wind equipment manufacturers.

The Importance of Industrial Policy in Wind Power Development

The Chinese government has been very adept at creating the conditions for the development of particular industries by setting goals, putting in place laws, regulations and policies, creating incentives, nurturing key enterprises, convening government agencies and enterprises to develop plans, while allowing market forces to flourish. Beijing’s nurturing of the wind power industry displays all of these propensities. An early November 2008 conference in Beijing convened by the National Energy Bureau demonstrates these forces at work. The key participants in the Chinese wind power industry from government and industry attended; these included representatives from the Pricing Department, the New Energy Department and the Planning Department of the National Development and Reform Commission, the State Power Grid Co., China Huaneng Group Co., China Datang Group Co., China Huadian Group Co., China Electric Power Investment Group Co., China Overseas Oil Co., China Hydropower Engineering Consulting Group Co., China Hydropower Construction Group Co., China Energy Conservation Investment Co., the Longyuan Power Group Co. (which at the end of 2007 became the first developer to exceed 1000 MW of installed wind power generating capacity), the Guohua Energy Investment Co., Ltd., the Beijing Capital Power International Energy Joint Stock Co., Ltd., etc., etc. Among the issues discussed was access to the power grid for wind power, the system for formulating power prices, the equipment manufacturing industry and the “special permitting” regime. Among other issues discussed was the need to both strengthen oversight and administration in wind construction planning and support systems at both the national and local levels for the construction of wind projects. With respect to incentivizing the development of the wind industry in China, in 2001 Beijing reduced the value-added taxes due on the production of wind power by one-half and in the eight months between October 2007 and June 2008 the Chinese government has provided approximately 1.4 billion Yuan (~$206 million U.S.D.) in financial subsidies for the wind industry; financial subsidies include a 600 Yuan/kw payment to domestic wind turbine and component manufacturers for the first 50 MW-class wind turbines that domestic wind turbine manufacturers produce. Industrial policy, including, importantly, the use of the “special permitting” process to select investors in wind farm development projects and utilize domestically produced equipment for the construction and operation of those wind farms has been a significant impetus to development of the wind industry in China. Beijing also has incentivized wind farm development through the requirement in the {Mid to Long Term Development Plan for Renewable Energy} that power generating companies that have an installed capacity of 5000 MW or more must produce non-hydropower renewable energy of at least 3% by 2010 and 8% by 2020. The support of the Chinese government to foster the construction of power grids that connect far flung centers of wind power production with the population and energy consumption centers on the coasts also is indispensable to the successful deployment of wind power in China. Some contend, though, that Beijing has fashioned a system, which creates an “indirect monopoly” for Chinese manufacturers that reduces competition and particularly disadvantages foreign manufacturers.

Addressing the Gaps in the Emerging System

Though progress has been substantial in the development of the Chinese wind industry, there continue to be gaps in the emerging wind power system that will need to be addressed. First, Beijing has not yet completed a policy for pricing wind power. The {Trial Measures for Renewable Energy Power Generation Pricing and Cost Sharing}, which were promulgated by the National Development and Reform Commission in 2006 provide for the on-grid price of wind power to be determined by the administrative department of the State Council in charge of pricing based on local conditions in accordance with the general principal of cost plus profit margin. Power pricing for wind power “special permitting” projects are to be determined by bid, but are not to exceed the level set by the administrative department of the State Council in charge of prices. Second, the development of power grids to serve the wind farm installations that are being constructed is lagging, causing difficulties in connecting and distributing power generated from wind farms that, in turn, results in waste. So while the {Measures Governing Purchases by Power Grid Companies of the Total Amount of Renewable Energy Generated}, promulgated in August 2007 provides a market for renewable energy, the lack of a fully developed grid makes that promise somewhat illusory. In 2007, for example, the State Power Grid Co. distributed only 1/10th (5 billion Kwh) of the potential total Kwhs that China’s wind farms theoretically were able to produce. Third, the technological level of domestic wind turbine manufacturers still needs to be improved and the quality of some of the domestic wind turbine components is not high.

Conclusion

In early November 2008 BP ended the cooperation that it began in January 2008 with Xinjiang Goldwind (Jinfeng) to build the 148.5 MW Inner Mongolia Damao Wind Power Project and withdrew its investment in the Asian wind power industry. At nearly the same time Japan’s Harakosan Co., Ltd. announced that it would sell its 27% interest in the Hara XEMC Wind Power Co., Ltd. to its joint venture partner XEMC, of Hunnan Province. Though these might be isolated cases, we suspect that the old trap of lower energy prices is tempting some to abandon the push towards greater reliance on wind power. The Chinese clearly are not taking the bait.

Lou Schwartz, president of China Strategies, LLC, and publisher of the China Renewable Energy and Sustainable Development Report, earned degrees in East Asian Studies from the University of Michigan and Harvard University where he studied Chinese language and literature, economics and law among other disciplines. Lou also earned a J.D. from George Washington University Law School. Fluent in Mandarin Chinese, Lou assists companies, non-profits and governments with various projects involving China’s legal system, economic development, trade and investment. Lou’s e-mail address is: lou@chinastrategiesllc.com

The international financial crisis, which has reverberated deeply into China’s economy, certainly has had an impact on the Chinese wind power sector in a number of ways. It has contributed to declining prices for certified emissions reduction credits (CERs) under the CDM Kyoto Protocol framework, a key subsidy for wind farm development, caused some foreign companies to exit the Chinese wind farm development business as oil prices have declined and credit has become more difficult to obtain and costly to acquire and brought on the recession that has resulted in declining energy use and falling power prices throughout China.

By most accounts, however, the impact of this worldwide financial upheaval has been limited with respect to China’s burgeoning wind power industry. In part this is attributable to the fact that the Chinese wind industry’s development is in large measure directed by Beijing and 80% of the market is concentrated in large state-owned enterprises. It is also due to the decision of the leadership in Beijing to forge ahead with renewable energy development as one element of its approach to combating the economic downturn China now faces. In fact, the centerpiece of Beijing’s response to the economic slowdown in China set off by the subprime mortgage breakdown is a $586 billion U.S. stimulus package, a quarter of which amount will be allocated to environmental, renewable energy and energy efficiency projects. Like the incoming Obama administration in the U.S., the Chinese government understands that they also can get a “two-fer” by funding renewable energy and energy efficiency projects that will both spur economic development and advance China towards its goal of a cleaner and more sustainable energy future (for every 1000 MW of wind power that is installed there is a reduction in carbon dioxide emissions of approximately 2.5 million tpy). So the silver lining in the clouds that darken the world’s economic landscape is that China appears more committed than ever to forge ahead with a robust program of renewable energy development, a key component of which is wind power development. That commitment already is being displayed; in the fourth quarter of 2008, of the 100 billion Yuan (~$14.8 billion U.S.D.) that the Chinese government is using to stimulate the economy through investment in renewable energy, a sizeable portion is being allocated to wind power projects.

Wind Power Will Be An Important Source of Power in China

While wind power in China now accounts for just 1.3% of total power output in China (compared with coal fired power at 75% of total power output), only three years ago wind power only accounted for 1/1000th of total power production in China. At the pace that installed capacity to produce power from the wind is being built in China, the contribution to total power needs from wind will continue to increase as the Chinese wind industry matures and the cost per Kwh to produce wind power continues to decrease. At the same time the restructuring of the power industry to reduce the number of small and disproportionately polluting coal-fired power plants will result in a more sustainable mix of power sources over time. China is making progress towards its plan to close a total of 50,000 MW of small, inefficient and highly polluting coal-fired power plants over the course of the 11th Five Year Plan Period (2006-2010); Beijing reports that through October 2008 it already has closed 32,100 MW of these offending power plants and plans to close an additional 13,000 MW of such small power plants in 2009. The process of rationalizing the coal-fired power plants in China is projected to save 40 million tpy of coal and reduce sulfur dioxide emissions and carbon dioxide emissions by, respectively, 680,000 tpy and 65 million tpy. Chinese planners envision a future mix of power generating sources totaling 1.2 million to 1.5 million MW (an average of 1KW/person/year), comprised on no more than 800,000 MW of coal-fired power plants, 200,000 to 300,000 MW of hydropower and wind power and 200,000 MW of nuclear energy.

The Accelerating Growth of Wind Power

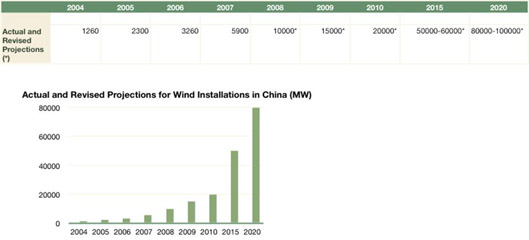

China’s wind energy potential is enormous. Chinese sources estimate that exploitable “wind resources” that are available on land in China may be as high as 600,000 to 1 million MW and that close-in off-shore exploitable wind power potential accounts for another 700,000 MW. Since the {Renewable Energy Law} took effect on January 1, 2006, China’s installed capacity to produce wind power has increased from 2300 MW as of the end of 2005, to in excess of 3200 MW as of the end of 2006, to 5900 MW as of the end of 2007 to more than 7000 MW as of mid-year 2008. Through the end of 2007 China had built more than 100 wind farms in 22 provinces and cities. China is on track to reach the symbolically important milestone of 10,000 MW of installed wind power as of the end of 2008—two years ahead of the revised goal. By 2010 cumulative installed capacity to produce wind power may reach 15,000 to 20,000 MW and after 2011 China will be adding new capacity at the rate of 7000-10,000 MW/year. By 2015 analysts predict that China’s base of wind power installations will total 50,000 to 60,000 MW and that by 2020 wind power will account for 80,000-100,000 MW of power generation in China; the goal for 2020 was revised upward four-fold from the 30,000 MW goal set by the {Mid to Long Term Development Plan for Renewable Energy} promulgated by Beijing in September 2007. (See accompanying chart). Central to this rapid development of wind power capacity in China is a series of ambitious mega-wind farm projects. There already are a series of such projects that are in planning (and at least one under construction) that should result in a total of approximately 100,000 MW of wind power by 2020 among only six mega-projects! These six large wind farm “bases” include 12,000 MW in Gansu Province; 20,000 MW in Hami in Xinjiang Province; 20,000 MW in Western Inner Mongolia; 30,000 MW in Eastern Inner Mongolia; 10,000 MW in Hebei Province; and 10,000 MW in Jiangsu Province.

As the third fastest growing wind power market in the world (after the U.S. and Spain) and the fifth largest installed base of wind power, in 2007 China attracted 15% of the world’s investment in wind power. According to Mr. Li Junfeng, the Vice-Chairman of the Energy Institute of the National Development and Reform Commission, in 2007 alone, China’s wind industry attracted investments totaling 34 billion Yuan (~$5 billion U.S.D.).

China’s Wind Power Equipment Manufacturing Industry

After several years of development, China’s wind power equipment manufacturing industry has now achieved a certain scale of operations and technological competence that will certainly help accelerate the development of wind power in China in the years ahead. Even with its rapid growth, however, the Chinese wind power equipment manufacturing industry is not yet keeping pace with demand. According to Chinese sources, there are now sixty-seven wind turbine manufacturers operating in China (up from 40 in mid 2007 and only 6 in 2004), including 27 state-owned or state controlled companies; 23 private companies; 8 joint venture companies and 9 wholly foreign-owned companies. Chinese wind turbine manufacturers in 2007 for the first time accounted for more than 50% (55.4%) of all wind turbines installed in China and because Chinese wind turbine manufacturers are now capable of producing 1.5 MW, 2 MW and now even 3 MW wind turbines, the expectation is that Chinese companies’ share of wind turbine installations will continue to increase. Though the numbers of wind turbine manufacturers have increased, the most significant Chinese competitors are Xinjiang Goldwind (Jin Feng) Science and Technology Joint Stock Co., Ltd., Dongfang and Sinovel Wind Power Science and Technology Co., Ltd. In the view of Han Junliang, the Chairman of Sinovel, the financial crisis will benefit the Chinese wind industry by hastening the consolidation of the wind turbine manufacturers. The percentage of wind turbines that are sourced domestically will increase as a consequence of the {Notice Concerning Certain Requirements for Wind Farm Construction Management}, which requires that 70% of the equipment sourced for any wind farm project must be sourced domestically. Tariff changes also have had the effect of supporting the development of the domestic wind turbine industry. On April 23, 2008 the Ministry of Finance announced the elimination, as of May 1, 2008, of tariff free importation of wind turbines that are less than 2.5 MW (tariff classification $85023100).

As more than 80% of the cost of a wind turbine is in the parts, the relatively quick development of an indigenous wind power equipment parts industry also is a sign of increasing maturity. The indigenous industry producing gearboxes, generators and blades is able to satisfy current demand in China, though the fact that there are now more than fifty of such companies presages intensified competition and perhaps the gradual appearance of these products on the export market. China remains largely dependent on imports for such key components as precision bearings, electrical and control systems and inverters. American Superconductor Corp. (AMSC), for example, has been enormously successful in selling its electrical and control systems to Chinese wind turbine manufacturers, such as Sinovel. To facilitate the import of components that are not being manufactured in China, as of January 1, 2008, the Ministry of Finance instituted a program of rebates of tariffs and VAT taxes paid on the importation of parts and raw materials used in the manufacture of wind turbines.

The development of an indigenous manufacturing base to support the growth of wind power installations in China promises to achieve the cost reductions that will continue to drive down the cost of this alternative energy source. Presently the cost of wind power is 0.5-0.6 Yuan/Kwh; the cost of thermal power from coal-fired power plants presently is 0.2-0.3 Yuan/Kwh. While only 19% of the 6458 wind turbines that were installed in China as of the end of 2007 were indigenously produced MW-class wind turbines, the pace of adoption of domestic wind turbines is increasing and this will increasingly result in significant cost savings for the industry. According to the Chinese, if 70% of wind turbines are manufactured locally, the cost of wind turbines can be reduced by 15% and without any other changes in cost structure, the reduced cost of wind turbines can result in a reduction in power generation costs to 0.375 Yuan/Kwh. If all wind turbines are manufactured domestically, the cost of wind turbines will decline a total of 30% and, again without any other cost savings factored in, the power generation costs of wind will decline to 0.332 Yuan/Kwh. Factoring in a cost associated with the pollution caused by coal fired power plants and the likelihood that fossil fuel prices will increase, the Chinese believe that they can achieve pricing parity between coal-fired power and wind power in the foreseeable future. The Chinese recognize that to achieve the cost reductions that will enable the industry to become cost competitive with coal-fired power plants, it will be imperative for them to invest, on average, 1.5-3% of the cost of a wind farm on science and technology research and development. In the short term the wind turbine industry will benefit from the drop in prices for steel and other materials used in the manufacture of wind turbines. As Chinese wind turbine manufacturing improves, the stage will be set for Chinese wind turbine and components manufacturers also to begin to export to the world.

Foreign wind power equipment manufacturers, including Denmark’s Vestas, India’s Suzlon, Spain’s Gamesa, Germany’s Nordex Corp. and GE Energy, aggressively have engaged the Chinese wind market. The spate of new wind turbine plants that foreign wind turbine manufacturers are building in China is a result of the explosive growth in wind power capacity development in China, but also a result of Chinese industrial policy that penalizes foreign imports and rewards domestically produced wind turbines. At 60 million Euros, Gamesa’s factory in Tianjin, which manufacturers wind turbines, is the Spanish company’s second largest foreign investment (after the U.S.) Nordex has located two of its three manufacturing centers in China and has established the company’s Asia headquarters in Beijing. Nordex expects to invest an additional 500 million Yuan (~$71 million U.S.D.) and grow its business in China four-fold in the next three years. Though foreign wind turbine manufacturers have a cumulative market share (total installed base) of the Chinese wind power equipment market of 65.9%, the inroads made by the emerging domestic Chinese wind turbine industry are evident in the fact that the foreign manufacturers market share of current installations has declined to 55.1%. The industrial policies of the Chinese government with respect to the emerging Chinese wind power industry—policies that have been described as “escorting the Emperor”—are contributing to the decline in market share of foreign manufacturers. The ability of Chinese companies to move more swiftly than foreign competitors to build factories and secure sales in China also contributes to the erosion of market share by foreign wind equipment manufacturers.

The Importance of Industrial Policy in Wind Power Development

The Chinese government has been very adept at creating the conditions for the development of particular industries by setting goals, putting in place laws, regulations and policies, creating incentives, nurturing key enterprises, convening government agencies and enterprises to develop plans, while allowing market forces to flourish. Beijing’s nurturing of the wind power industry displays all of these propensities. An early November 2008 conference in Beijing convened by the National Energy Bureau demonstrates these forces at work. The key participants in the Chinese wind power industry from government and industry attended; these included representatives from the Pricing Department, the New Energy Department and the Planning Department of the National Development and Reform Commission, the State Power Grid Co., China Huaneng Group Co., China Datang Group Co., China Huadian Group Co., China Electric Power Investment Group Co., China Overseas Oil Co., China Hydropower Engineering Consulting Group Co., China Hydropower Construction Group Co., China Energy Conservation Investment Co., the Longyuan Power Group Co. (which at the end of 2007 became the first developer to exceed 1000 MW of installed wind power generating capacity), the Guohua Energy Investment Co., Ltd., the Beijing Capital Power International Energy Joint Stock Co., Ltd., etc., etc. Among the issues discussed was access to the power grid for wind power, the system for formulating power prices, the equipment manufacturing industry and the “special permitting” regime. Among other issues discussed was the need to both strengthen oversight and administration in wind construction planning and support systems at both the national and local levels for the construction of wind projects. With respect to incentivizing the development of the wind industry in China, in 2001 Beijing reduced the value-added taxes due on the production of wind power by one-half and in the eight months between October 2007 and June 2008 the Chinese government has provided approximately 1.4 billion Yuan (~$206 million U.S.D.) in financial subsidies for the wind industry; financial subsidies include a 600 Yuan/kw payment to domestic wind turbine and component manufacturers for the first 50 MW-class wind turbines that domestic wind turbine manufacturers produce. Industrial policy, including, importantly, the use of the “special permitting” process to select investors in wind farm development projects and utilize domestically produced equipment for the construction and operation of those wind farms has been a significant impetus to development of the wind industry in China. Beijing also has incentivized wind farm development through the requirement in the {Mid to Long Term Development Plan for Renewable Energy} that power generating companies that have an installed capacity of 5000 MW or more must produce non-hydropower renewable energy of at least 3% by 2010 and 8% by 2020. The support of the Chinese government to foster the construction of power grids that connect far flung centers of wind power production with the population and energy consumption centers on the coasts also is indispensable to the successful deployment of wind power in China. Some contend, though, that Beijing has fashioned a system, which creates an “indirect monopoly” for Chinese manufacturers that reduces competition and particularly disadvantages foreign manufacturers.

Addressing the Gaps in the Emerging System

Though progress has been substantial in the development of the Chinese wind industry, there continue to be gaps in the emerging wind power system that will need to be addressed. First, Beijing has not yet completed a policy for pricing wind power. The {Trial Measures for Renewable Energy Power Generation Pricing and Cost Sharing}, which were promulgated by the National Development and Reform Commission in 2006 provide for the on-grid price of wind power to be determined by the administrative department of the State Council in charge of pricing based on local conditions in accordance with the general principal of cost plus profit margin. Power pricing for wind power “special permitting” projects are to be determined by bid, but are not to exceed the level set by the administrative department of the State Council in charge of prices. Second, the development of power grids to serve the wind farm installations that are being constructed is lagging, causing difficulties in connecting and distributing power generated from wind farms that, in turn, results in waste. So while the {Measures Governing Purchases by Power Grid Companies of the Total Amount of Renewable Energy Generated}, promulgated in August 2007 provides a market for renewable energy, the lack of a fully developed grid makes that promise somewhat illusory. In 2007, for example, the State Power Grid Co. distributed only 1/10th (5 billion Kwh) of the potential total Kwhs that China’s wind farms theoretically were able to produce. Third, the technological level of domestic wind turbine manufacturers still needs to be improved and the quality of some of the domestic wind turbine components is not high.

Conclusion

In early November 2008 BP ended the cooperation that it began in January 2008 with Xinjiang Goldwind (Jinfeng) to build the 148.5 MW Inner Mongolia Damao Wind Power Project and withdrew its investment in the Asian wind power industry. At nearly the same time Japan’s Harakosan Co., Ltd. announced that it would sell its 27% interest in the Hara XEMC Wind Power Co., Ltd. to its joint venture partner XEMC, of Hunnan Province. Though these might be isolated cases, we suspect that the old trap of lower energy prices is tempting some to abandon the push towards greater reliance on wind power. The Chinese clearly are not taking the bait.

Lou Schwartz, president of China Strategies, LLC, and publisher of the China Renewable Energy and Sustainable Development Report, earned degrees in East Asian Studies from the University of Michigan and Harvard University where he studied Chinese language and literature, economics and law among other disciplines. Lou also earned a J.D. from George Washington University Law School. Fluent in Mandarin Chinese, Lou assists companies, non-profits and governments with various projects involving China’s legal system, economic development, trade and investment. Lou’s e-mail address is: lou@chinastrategiesllc.com

You can return to the main Market News page, or press the Back button on your browser.